Why Enterprise AI Governance Is Building the Weapon That Will Destroy Companies, Boards, and Shareholders

Executives Are in Breach of Fiduciary Duty by Deploying Ungoverned Enterprise AI — D&O Exclusions Are Already Proving It, and the EU AI Act’s Imminent Enforcement Will Accelerate the Carnage

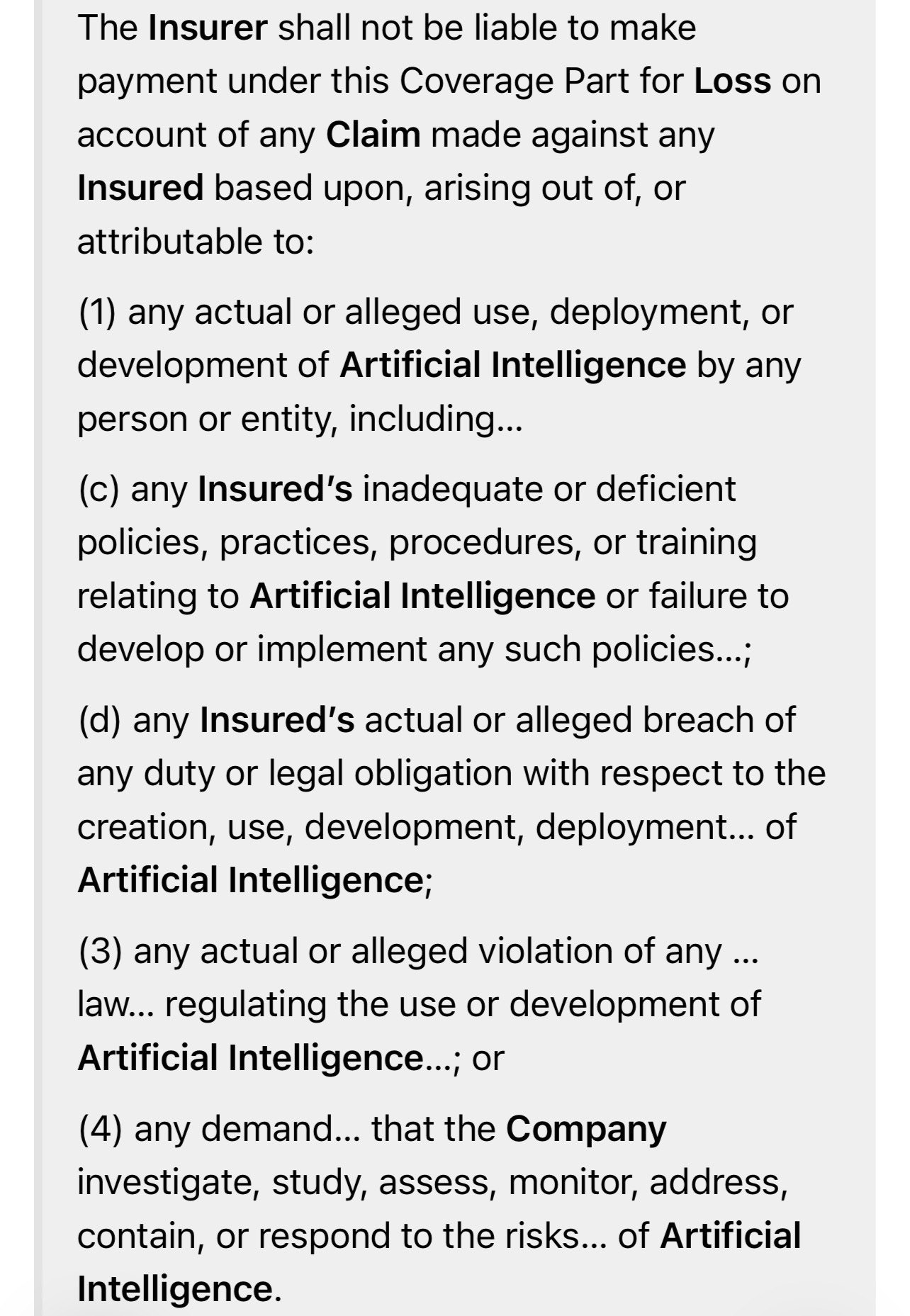

Actual excerpt from a D&O Policy.

By David P. Reichwein, CEO AI²

May 2026

Fortune 500 executives and boards are not merely negligent.

They are in active breach of their fiduciary duties by implementing ungoverned — or theater-governed — enterprise AI at scale.

They are forging weapons that plaintiffs, regulators, activist shareholders, and now their own insurerswill use to dismantle companies, crush market caps, and impose personal liability.

The evidence is already written into the insurance policies.

Part I: Fiduciary Breach in Real Time

Fiduciary responsibility — duty of care, loyalty, and good faith — requires boards to exercise prudent oversight of material risks. Deploying probabilistic AI into high-stakes domains (healthcare, finance, autonomous operations, legal decisioning) with nothing but prompt wrappers, RAG monitors, and consultant decks violates that duty.

This is the Authorization Gap™: probabilistic tools policing probabilistic systems in the same runtime. Bad outputs execute. Boards approving this while ignoring architectural independence are reckless, not reasonable.

Every green dashboard, risk memo admitting “residual probabilistic risk,” and “responsible AI” policy is not protection — it is a confession of foreseeability. This creates the cleanest audit trail in corporate history for Caremark claims (breach of oversight duties).

Part II: D&O Insurance Is Already Abandoning You

Insurers see the bloodbath coming and are exiting the theater — now.

Major carriers, led by W.R. Berkley, have introduced “Absolute AI Exclusions” in D&O (and E&O/fiduciary) policies starting in late 2025 and rolling aggressively into 2026. One of the clearest examples is Berkley Form PC 51380, which contains this sweeping language:

The Insurer shall not be liable to make payment under this Coverage Part for Loss on account of any Claim made against any Insured based upon, arising out of, or attributable to:

(1) any actual or alleged use, deployment, or development of Artificial Intelligence by any person or entity, including…

(c) any Insured’s inadequate or deficient policies, practices, procedures, or training relating to Artificial Intelligence or failure to develop or implement any such policies…;

(d) any Insured’s actual or alleged breach of any duty or legal obligation with respect to the creation, use, development, deployment… of Artificial Intelligence;

(3) any actual or alleged violation of any … law… regulating the use or development of Artificial Intelligence…; or

(4) any demand… that the Company investigate, study, assess, monitor, address, contain, or respond to the risks… of Artificial Intelligence.

The definition of Artificial Intelligence is deliberately broad, covering virtually any inferential system that generates predictions, content, recommendations, or decisions.

Result? Boards relying on software-only “governance” discover their D&O coverage — the last line of defense against personal liability — evaporates precisely when failures hit. Premiums spike, limits shrink, and underwriters now aggressively grill on AI oversight at renewal. Weak or theater-based governance equals exclusions or outright declinations.

This is the insurance market explicitly telling you what your fiduciary duty demands: real architecture, not probabilistic theater. Ignoring it breaches your duty and leaves directors personally exposed.

Part III: The Self-Inflicted Weapon

Current “probabilistic governance” does not mitigate risk. It manufactures prosecution exhibits while voiding insurance. Consultants billing for prompt engineering decks are arming plaintiffs and handing insurers ready-made grounds for denial.

Shareholders pay the price: massive uncovered losses, stock drops, derivative suits. The pattern from asbestos, tobacco, and opioids is repeating — faster, with digital evidence, and now with insurers already bailed out.

Part IV: The Actuarial Bloodbath

Expected Annual Liability (EAL) = N_d × P_bad × P_exec|bad × (L_direct + F_reg + R_rep + ΔMarketCap + Uncovered_D&O)

Add uncovered personal exposure for directors and officers and the numbers become existential. High-stakes AI generates millions of decisions daily. P_exec|bad stays near-certain in software-only setups. EU fines and torts land uninsured on the balance sheet.

Part V: The EU AI Act — The Reckoning Accelerant

Enforcement deadlines are fast approaching and will expose these failures:

February 2025 (passed): Prohibited practices locked.

August 2025 (passed): GPAI obligations active.

August 2026 (months away): Full high-risk systems enforcement (Annex III) — mandatory independent risk management, conformity assessments, oversight.

2027+: Legacy systems, enforcement actions, precedents.

Fines up to 7% of global turnover. Article 9 demands independent controls. Software guardrails co-located with the AI fail this test. Non-compliance triggers uncovered D&O claims and personal liability. Time is running out.

Part VI: Software Cannot Govern Software

Nuclear, aviation, and process control industries learned decades ago to use deterministic safeguards. AI’s cheap software-only delusion is ending. D&O exclusions are the market’s verdict on theater governance.

Part VII: The Defensible Path — Close the Gap

Permission Control Runtime (PCR™) + Quadzistor™ hardware enforcement provides true independence: separate runtime, cryptographic permissions, physical blocking, external immutable logs.

P_exec|bad collapses. Defensibility soars. This satisfies EU Article 9, strengthens Caremark compliance, and materially improves insurability. This is what actual fiduciary care looks like in the age of agentic AI.

Part VIII: The Shareholder Call to Action

To boards and executives: You are in breach by deploying ungoverned AI. The Berkley Absolute AI Exclusion and similar policies prove the market already knows it. Stop forging your own destruction.

To shareholders, activists, and institutional investors: Demand accountability now.

Honest EAL models including uncovered D&O exposures.

Proof of independent architectural controls surviving EU scrutiny and discovery.

Real adversarial P_exec|bad testing.

Full policy audits for AI exclusions (read the endorsements — they’re buried).

The Authorization Gap™ is sitting on your balance sheet as unrecognized liability. Leadership implementing theater is breaching fiduciary duty. The EU AI Act deadlines make denial impossible. The first major incident will trigger the wave — with insurers already sidelined.

Close the Gap with real engineering. Inform shareholders transparently. Fulfill the duty you owe — before verdicts and exclusions prove the breach in open court.

The green dashboards and consultant decks will not save you. The evidence you created — and the insurance you lost — will condemn you.

Shareholders: Get informed. Get demanding. The weapon is armed. The time is now.