AI2 Global Intelligence Brief

June 13, 2026

The Metric That Matters

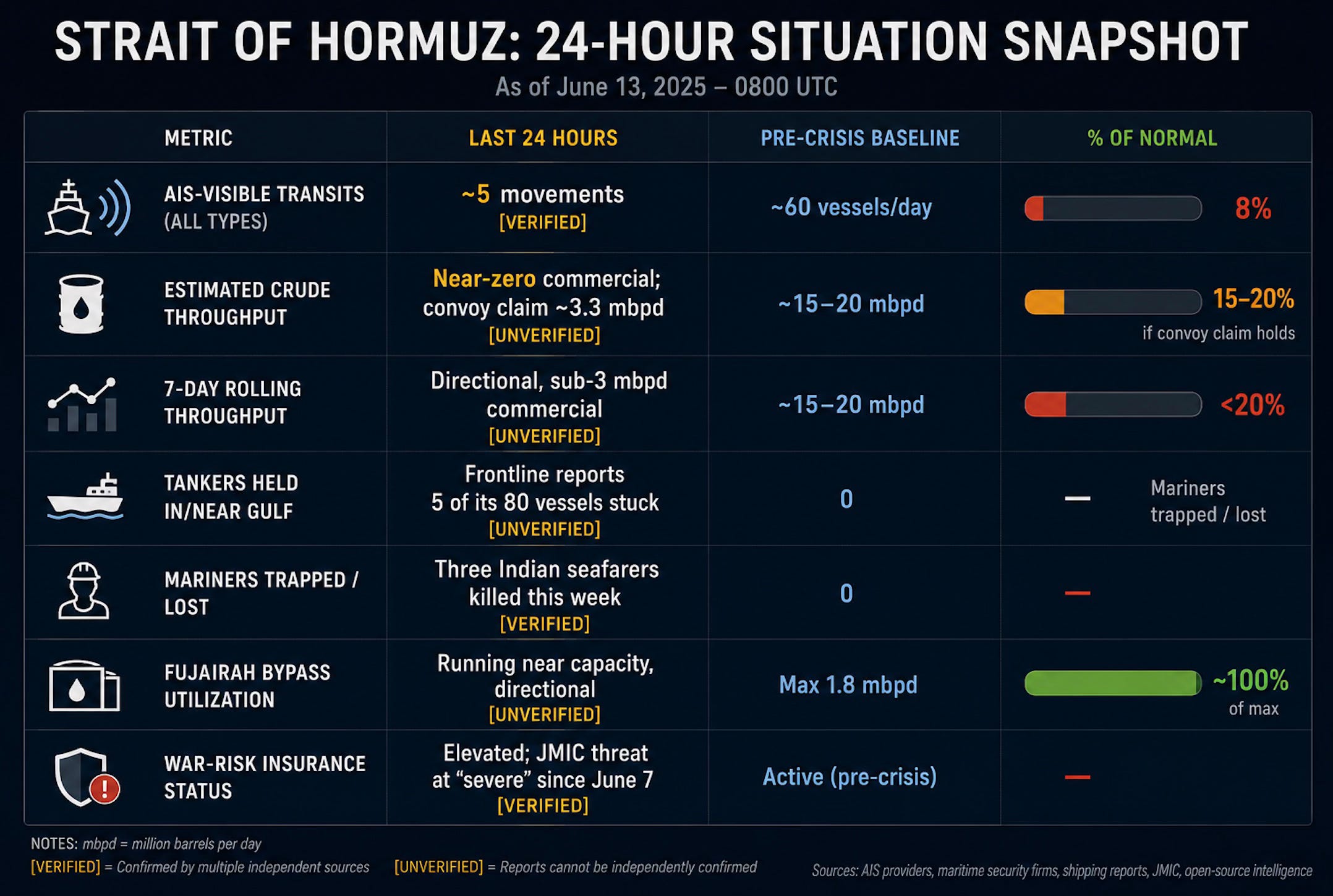

Tanker Flow — Last 24 Hours

Read this before anything else. The diplomatic headline says the war is ending. The water says something slower.

—

Gross vs. net. Gross Hormuz throughput remains effectively halted against a 15–20 mbpd baseline, yet the net shortfall reaching global markets is a fraction of that — absorbed by shadow-fleet routing along the Iranian and southern Omani corridors, SPR draws, the Fujairah bypass, and Cape rerouting. The gap between the gross stoppage and the net shortfall is the entire story.

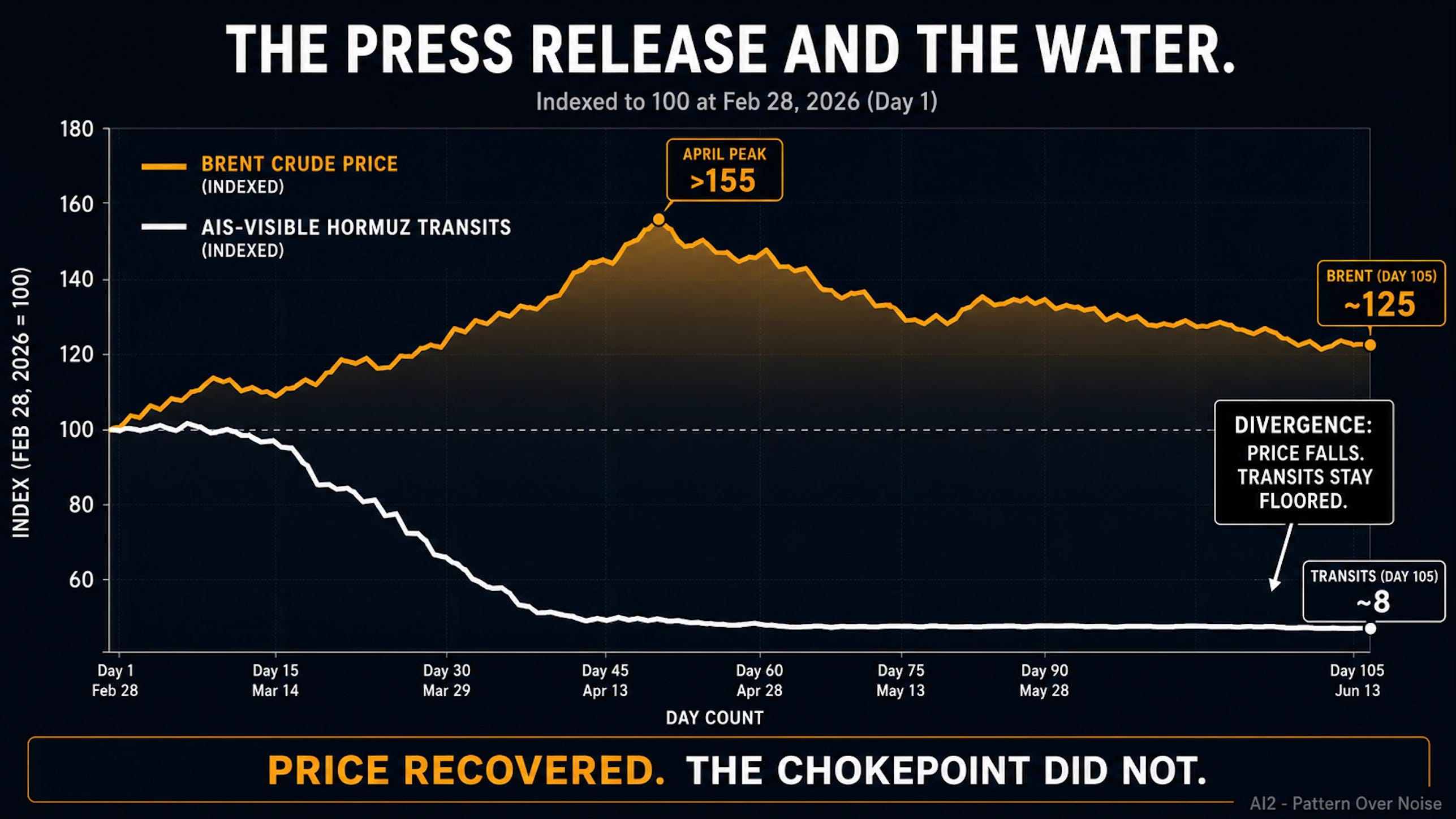

Gap direction. Narrowing. Brent fell to an eight-week low this week as the workaround economy normalized and Pakistan’s prime minister confirmed a “final, agreed upon text” — the driver is diplomatic, not physical.

What the flow shows. Physical transits sit near five a day while Brent trades around $87 and the S&P 500 sits near 7,430 — price and equities are tracking the press release, not the water. That is divergence, and it is the trade.

The 90-Second Brief

Three numbers, one pattern

~5

Hormuz transits a day vs. ~60 baseline

$87

Brent, an eight-week low, down from $110+ in April

7,430

S&P 500, within reach of records

The pattern: the market has fully repriced the war as over while the chokepoint it depends on is still moving at eight percent of normal capacity.

The forward implication: a signed memorandum reopens the legal status of the strait long before it reopens the physical flow — mines, idled fields, and repositioned tankers are measured in weeks, not headlines.

The full eight-domain architecture is in the Pattern Signal Matrix below.

The One Pattern That Matters Today

Signature ahead of the ship

Pakistan’s prime minister announced a “final, agreed upon text” of a US–Iran deal, and Brent collapsed to an eight-week low near $87 while the S&P 500 pushed toward 7,430. But AIS-visible Hormuz transits held near five a day — about eight percent of the pre-war norm — and CENTCOM was still downing Iranian drones over the strait the same evening.

The market is pricing the press release; the water is still pricing the war.

That distance between what Washington and Tehran have verbally authorized and what the strait physically enforces is the Authorization Gap™ rendered in crude oil and basis points.

Hero Image PromptCinematic editorial illustration, premium newsroom cover aesthetic in the register of a Foreign Affairs or Bloomberg Businessweek cover. Central metaphor: a single oil tanker frozen mid-channel in a narrow dark strait, while above it a luminous paper document dissolves into light — the signature racing ahead of the ship that cannot yet move. Dark slate-and-charcoal palette with one accent of warm amber catching the document’s edge. High tonal contrast for thumbnail legibility. No text, no logos, no readable signage. 16:9, 8K. Internal caption: “the signature and the ship.”

The Top 20 Stories

What the headlines mean

Story 1 — “Final, agreed upon text” reached on a US–Iran deal

What happenedPakistan’s prime minister Shehbaz Sharif said the text of a US–Iran agreement has been settled, and Trump said it could be signed over the weekend in Europe with Vice President JD Vance attending.

Why it mattersA memorandum of understanding would reopen the strait, extend the ceasefire 60 days, lift the US port blockade, and lock Iran into a non-weapons commitment — the architecture that has moved every market in this brief.

Hidden driverTrump needs the inflation relief before the November midterm window opens, and Tehran needs sanctions relief and frozen funds — both clocks point at a deal, not the war.

Story 2 — Iran’s own framing contradicts the “reopening” narrative

What happenedIran’s IRNA stated the text contains no commitment to cede management of the strait, and Foreign Minister Araghchi said transiting ships will pay “service fees,” not tolls.

Why it mattersWashington is selling immediate, free reopening; Tehran is describing a managed waterway it still controls and monetizes. The same document is being read two ways, which is how ceasefires unravel.

Hidden driverControl of Hormuz is Iran’s last leverage after losing the air war — it will not surrender the one card that survived.

Story 3 — Brent and WTI hit eight-week lows

What happenedBrent traded near $87 for August and WTI closed under $85 for July, down roughly 4% on the day and far below the $110-plus April peak.

Why it mattersCrude is pricing a resolution that has not physically occurred, with transits still floored. The price is a bet on the signature, not a reflection of barrels moving.

Hidden driverThe workaround economy — shadow fleet, Fujairah, Cape rerouting — quietly capped the price months ago, so deal optimism is removing a risk premium the physical market had already partly defused.

Story 4 — Strikes continue even as diplomacy closes

What happenedCENTCOM downed multiple Iranian attack drones near Hormuz on Friday evening; the mid-April ceasefire has effectively collapsed twice, with both sides resuming fire this week.

Why it mattersA “final text” coexisting with live drone intercepts is the definition of an unstable equilibrium. The market is treating kinetic events as noise around an assumed deal — dangerous if Mojtaba Khamenei’s final sign-off slips.

Hidden driverEach side is fighting to set the baseline the agreement freezes; the violence is negotiation by other means.

Story 5 — Tanker flow remains near a standstill

What happenedAIS-visible transits ran to roughly five movements over June 10–11, among the lowest since the conflict began, while Trump claimed the Navy secretly escorted 200 ships and 100 million barrels over the past month.

Why it mattersEven taking the escort claim at face value, that is a managed trickle, not a functioning chokepoint. The Frontline CEO estimates about half of moving vessels use the Iranian route and half the southern Omani corridor.

Hidden driverRepositioning idled tankers — not signing paper — is what Aramco and Frontline both name as the real bottleneck to restoring flow.

Story 6 — SpaceX completes the largest IPO on record

What happenedSpaceX priced at $135, opened at $150, and closed near $161, up about 19%, raising roughly $75 billion earmarked for data-center and compute expansion.

Why it mattersA single private company just pulled $75 billion of capital toward compute infrastructure, and AI-infrastructure names wavered on the print — the market is rotating capital, not just adding it.

Hidden driverCapital is front-running the buildout of the physical layer of AI before the energy constraint on that layer is priced.

Story 7 — ECB raises rates for the first time since 2023

What happenedThe European Central Bank hiked on Thursday and revised its 2026 and 2027 inflation forecasts higher.

Why it mattersA central bank tightening into a war-driven energy shock signals that inflation, not growth, is the dominant fear in Europe. It pressures gold and tightens the runway for energy-exposed industry.

Hidden driverImported energy inflation has overtaken demand weakness as the ECB’s binding constraint — a stagflationary posture, not a growth one.

Story 8 — Gold falls roughly 10% on the month despite the war

What happenedGold trades near $4,200, down about 10% from its January peak above $5,000, with silver around $74.

Why it mattersA safe-haven asset declining during an active Middle East war is a correlation break worth flagging — rate expectations are overpowering geopolitical fear. Markets have priced out 2026 Fed cuts and some now price a hike.

Hidden driverWith the Fed “trapped” between hot CPI and a war shock, real-yield expectations are setting the gold price, not the tankers.

Story 9 — Chip stocks sold off hard, then stabilized

What happenedThe Nasdaq fell 4.18% on June 4, its worst day since April 2025, after Broadcom failed to raise its AI chip outlook; the index has since clawed back.

Why it mattersThe AI trade is now sensitive enough that a single guidance miss erases a year’s worth of single-day moves. It exposes how much of the index rests on continued semiconductor acceleration.

Hidden driverThe market treats any deceleration in AI-capex guidance as a regime question, not a quarter — the multiple cannot survive a plateau.

Story 10 — India and China scramble for the same scarce barrels

What happenedWith Gulf supply disrupted, India and China are competing intensely for Russian crude, and India imported its first Iranian oil in seven years.

Why it mattersThe two largest Asian importers are bidding against each other for a shrinking pool of non-Hormuz supply, which props up Russian crude demand and Moscow’s revenue.

Hidden driverAlmost all sanctioned Iranian crude flows to China; India’s pivot to Iranian and Russian barrels is survival, not alignment.

Story 11 — US disables Iranian-linked tankers; Kharg terminals empty

What happenedUS forces disabled the M/T Settebello and M/T Jalveer in the Gulf of Oman, and both crude terminals at Kharg Island stood empty for the first time since early June.

Why it mattersEmpty Kharg terminals mean Iran’s primary export node is effectively offline, deepening the supply hole even as a deal is announced.

Hidden driverEach disabled vessel raises the insurance and repositioning cost of the eventual restart — the damage compounds the reopening timeline.

Story 12 — US inflation at multi-year highs

What happenedUS inflation has been pushed to its highest level in years by the energy shock, with CPI running hot.

Why it mattersThis is the political fuel behind the deal urgency — every week of $90 crude is a week of pump-price pain ahead of the midterms.

Hidden driverThe administration’s foreign-policy clock is set by the consumer price index, not the battlefield.

Story 13 — JMIC downgrades the Hormuz threat to “severe”

What happenedThe Joint Maritime Information Center cut its threat assessment from critical to severe on June 7, citing safe transits via the southern Omani route.

Why it mattersA downgrade, not an all-clear — shipowners read “severe” as still-uninsurable for most commercial transits. The Frontline CEO says flow returns fast only when red lights turn orange.

Hidden driverInsurance underwriters, not governments, will decide when the strait reopens in practice.

Story 14 — Nvidia and TSMC deepen fab-level AI integration

What happenedOn June 1, Nvidia and TSMC announced TSMC’s use of Nvidia’s accelerated computing and AI models across lithography, defect inspection, and wafer scheduling.

Why it mattersThe dominant chip designer and the dominant foundry are fusing AI into the manufacturing layer itself, tightening an already concentrated supply chain.

Hidden driverYield, not design, is now the scarce resource — and both firms are racing to automate the one bottleneck money cannot quickly buy.

Story 15 — Hyperscaler capex approaches $700 billion

What happenedAggregate hyperscaler capital spending is approaching $700 billion, with SpaceX’s $75 billion raise adding to the compute pipeline.

Why it mattersThis is the demand side of the compute-energy collision — three-quarters of a trillion dollars chasing power and silicon the grid cannot yet supply.

Hidden driverThe buildout is being financed faster than the electricity to run it is being permitted.

Story 16 — Three Indian seafarers killed near Hormuz

What happenedA strike near the strait killed three Indian seafarers, drawing IMO condemnation and a UN Secretary-General warning on shipping safety.

Why it mattersCivilian maritime casualties raise the war-risk premium and harden crew-supply shortages, an underpriced constraint on any reopening.

Hidden driverCrews, not hulls, may become the binding shortage — insurers can replace a ship faster than owners can crew one into a war zone.

Story 17 — US indices hold near records on the deal bid

What happenedThe Dow closed near 51,200 and the Russell 2000 led gains earlier in the week, with the VIX easing toward 19.

Why it mattersSmall-cap leadership and a falling volatility index signal a market positioned for resolution and lower rates — a posture vulnerable to any deal slippage.

Hidden driverThe index is long the ceasefire; a collapsed sign-off is the unhedged tail.

Story 18 — Iran’s leadership transition shapes the endgame

What happenedWith the supreme leadership now under Mojtaba Khamenei following the February assassination of Ali Khamenei, a senior US official said Iran’s leader is “comfortable” with the negotiations.

Why it mattersThe deal’s last missing piece is a single sign-off from a new and untested leader — the entire market repricing rests on one man’s signature.

Hidden driverA new supreme leader cannot afford to look like he surrendered the strait, which is precisely why the “service fees” framing exists.

Story 19 — OPEC+ and Gulf producers position for a reopening surge

What happenedOPEC+ raised quotas earlier in the crisis, and Gulf producers have pre-positioned tankers near Hormuz to export the moment it reopens.

Why it mattersA wall of pent-up supply sits behind the chokepoint, which means a credible reopening could overshoot to the downside on price.

Hidden driverThe supply bottled up for 105 days does not vanish — it queues, and queues unwind violently.

Story 20 — The frozen-funds test of trust

What happenedIranian officials have framed the release of roughly $24 billion in frozen Iranian funds as a precondition test of US good faith.

Why it mattersMoney, not missiles, is now the gating item — sanctions relief and asset release are the deal’s load-bearing terms.

Hidden driverBoth sides have already decided to settle; the remaining fight is over the price of the settlement.

Synthesis

The System Map

Five forces are setting the field. A physical chokepoint is throttling 15–20 mbpd of nominal flow to a managed trickle. A diplomatic track has produced a text that both capitals read differently. A monetary regime — hot US inflation, an ECB hike, priced-out Fed cuts — is overpowering geopolitical fear in gold and rates. A capital wave near $700 billion is pulling toward compute faster than the grid can feed it. And an electoral clock in Washington, with the midterms five months out, is pressing the President toward a fast resolution regardless of whether the water is ready.

Pattern Recognition

What is accelerating: the divergence between paper resolution and physical capacity. What is breaking: the safe-haven bid in gold, severed by rate expectations. The repeating political structure is the deadline-and-extension cycle — Trump has set ultimatums, watched ceasefires collapse, and reset them, producing the same outcome each time: managed de-escalation without restored flow. The pattern that should worry the market is that every prior “deal is close” moment this spring preceded another round of strikes.

Historical Anchoring

The closest analog is the 1987–88 Tanker War, not the 1973 embargo. In 1987, the US reflagged and escorted Kuwaiti tankers through a contested Hormuz under continuous low-level Iranian harassment — exactly the convoy posture Trump now describes with his 200-ship escort claim. The 1973 embargo was a deliberate supply cutoff; this is a contested-transit war where flow is throttled by risk and insurance, not by a producer’s decision. Where it diverges: in 1987 there was no compute-energy demand layer and no shadow fleet of this scale, so the price signal today is muffled in a way it was not then.

Forward Projection

If the text is signed this weekend, expect a legal reopening within days and a physical restart measured in weeks — mine clearance, restarting idled fields, repairing damaged facilities, and repositioning tankers each add latency. The shortest runway is fiscal-political, not military: the US inflation clock and the midterm calendar pull harder than any battlefield consideration, which is why a deal is likely even on shaky terms. The second-order risk is a downside oil overshoot as bottled-up OPEC+ and Gulf supply unwinds into a market that has already removed its risk premium. If the sign-off slips, the repricing reverses violently because the market is positioned long the resolution.

The Local Lens

United States — Pump-price inflation is the binding domestic constraint, and with no national election inside the 90-day window, the President holds unusual latitude to sign a contested deal before the August Generic Ballot hardens the midterm narrative. California’s refining system, heavily configured for Gulf grades, is the most structurally exposed state to any reopening delay.

Europe — The ECB’s hike into an energy shock signals industrial pain ahead; energy-import costs are squeezing competitiveness and the incumbents carrying them. Alliance cohesion holds, but the inflation revision tells you Frankfurt expects the shock to persist.

Asia — China absorbs almost all sanctioned Iranian crude and is bidding against India for Russian barrels, converting the crisis into cheap supply and leverage. Japan and South Korea remain the strategic hostages of any Hormuz or Taiwan disruption, with no domestic energy fallback.

Middle East — Gulf producers have pre-positioned to flood the market on reopening, while Iran’s new leadership monetizes the strait through “service fees” to avoid the appearance of surrender. The post-war regional order is being written in the gap between those two postures.

India — Energy arbitrage: India is extracting discounted Russian crude (historically $8–10 under Brent on delivered terms) and has restarted Iranian imports for the first time in seven years, cushioning a terms-of-trade hit from elevated Gulf prices. Refined-product export dynamic: refiners run Russian and Iranian feedstock to protect gross margins on diesel and gasoline exports westward. Strategic-ambiguity dividend: this week New Delhi sourced barrels simultaneously from Russia, Iran, and the Gulf while keeping its US trade track alive — extracting supply security from four mutually hostile relationships at once. Domestic exposure: imported-energy inflation is the political risk, with three Indian seafarers killed this week sharpening the security debate. Semiconductor and AI positioning: India remains a downstream assembler, more exposed to the compute-energy cost curve than positioned to profit from it, little changed from six months ago. Ambiguity risk: the US–India track is most likely to force a declared position, given Washington’s on-again, off-again Russian-crude waivers.

Global South — Watch the energy-importing frontier economies absorbing $90 crude with weak currencies; debt-service and FX stress is building quietly beneath the Hormuz headlines, the kind of slow pressure that surfaces as a balance-of-payments event one quarter late.

The Blind Spot Check

This brief has leaned hard on the assumption that a signed text means de-escalation. The embedded assumption most likely wrong is that Mojtaba Khamenei’s sign-off is a formality — a new supreme leader rejecting a deal that looks like capitulation is a live scenario the market is not pricing. The uncovered story the pattern says matters: crew shortages. Insurers can replace hulls; owners cannot quickly crew ships into a strait where seafarers are dying, and that human bottleneck may outlast the diplomatic one.

Before the line

You have just read the surface layer. Today that surface is roughly five Hormuz transits a day, Brent near $87, an S&P near 7,430 — and the pattern is already uncomfortable from here, because none of those three numbers agree with the other two.

Below the line is the full eight-domain Pattern Signal Matrix: the macro pressure field, the gold correlation break, the energy workaround economy quantified, a twenty-commodity scan, the equity and AI-hardware signal, and the Political Signal Watch reading the constraint sets on every decision-maker in this crisis — including the new Iranian leader holding the one structural veto the market has priced as a formality. It closes with the Divergence Flag: the single place consensus is most wrong today, stated without hedging.

The free section shows you the dislocations. The paid section tells you what closes them, what breaks first, and what the market will keep getting wrong for at least one more quarter.

And here is the bridge: the Authorization Gap™ is not only an AI-governance framework — it is the operating logic of every crisis in today’s brief. The gap between what actors claim is happening and what the pattern reveals is happening is where the next move originates.

In The Authorization Gap™, David P. Reichwein exposes why probabilistic AI systems cannot govern themselves and delivers the deterministic, hardware-enforced control architectures — Quadzistor™, PCR™, and pre-execution permission gates — required to close the gap between capability and authorized action before autonomous systems make the next irreversible decision. a.co/d/0d4PGVOB

Continue below.

Pattern Signal Matrix · Paid Analysis ( Gratis Today )

Reading signal from noise

This section issues no forecasts and no financial advice. It reads patterns. The data exists; the noise is overwhelming; the Matrix filters signal from noise.

Part One — Macro Geopolitical Pattern Header

The dominant pressure field is four simultaneous compressions. A physical-supply compression: Hormuz throughput throttled to roughly eight percent of normal — intensifying, with Kharg terminals empty. A monetary compression: an ECB hike, priced-out Fed cuts, multi-year-high US inflation — holding tight. A diplomatic compression: a “final text” with contradictory readings between Washington and Tehran — releasing, but unstably. A capital compression: near $700 billion of hyperscaler capex chasing scarce power and silicon — intensifying.

Apply the chokepoint standard: gross flow halted against 15–20 mbpd; net shortfall a fraction of that after shadow-fleet routing, SPR draws, the Fujairah bypass, and Cape rerouting; the gap reveals a system absorbing a total-stoppage shock at a manageable price — which is exactly why complacency is the risk. The 24-hour flow figure of roughly five transits is contradicting the price signal: Brent says the crisis is ending; the water says it has not started reopening. The sharpest macro divergence today is Brent falling while physical transits stay floored. Every signal below is read against this field.

Part Two — Gold and Precious Metals

Gold near $4,200 — distribution off the January high above $5,000. Patterns indicate → downside pressure as real-yield expectations rise, driver the ECB hike and a Fed pricing out cuts.

Silver near $74 — compression with an industrial-demand floor. Patterns indicate → relative resilience versus gold on electronics and solar pull.

Platinum and palladium — inflection, autocatalyst demand soft. Patterns indicate → continued underperformance.

Copper, the macro signal metal — holding, torn between AI-grid buildout demand and recession fear. Patterns indicate → a coiled range.

The flagged correlation break: gold is falling during an active war. Safe-haven demand has been overwhelmed by rate expectations — the metal is trading the Fed, not the strait. That break is among the highest-conviction signals in the Matrix this week.

Part Three — Energy Complex

Brent ~$87 (Aug), eight-week low. Patterns indicate → a risk premium unwinding ahead of physical confirmation.

WTI <$85 (July). Patterns indicate → the same de-escalation bet, one grade west.

European TTF gas — directional; structurally bid on supply anxiety. Patterns indicate → a persistent premium.

Henry Hub, LPG, coal — directional, firm on substitution demand.

The most important energy signal today: Brent is not reflecting the gross disruption figure. The gap between a halted chokepoint and an $87 print is the workaround economy suppressing the price signal — shadow-fleet volume routing through the Iranian and southern Omani corridors (roughly split fifty-fifty per Frontline), SPR drawdowns running on a runway best treated as weeks rather than months, the Fujairah bypass near its 1.8 mbpd ceiling, and Cape rerouting adding days and dollars per voyage. The workaround economy is the energy signal, not a footnote — and it is precisely what a reopening surge would render redundant, which is the downside-overshoot risk.

Part Four — Top 20 Commodities Signal Scan

Directional this session; price points are structural reads, not verified ranges.

AGRICULTURAL VECTORS

Wheat — → firm on Black Sea freight risk, watch Russian export pace.

Corn — → range-bound, US planting weather the swing factor.

Soybeans — → soft, China demand the dominant tell.

Rice — → elevated on Asian export controls, India the actor.

Sugar — → firm on Brazilian cane and energy-linked ethanol pull.

Coffee — → tight, Brazil and Vietnam weather-driven.

Cocoa — → structurally bid, West African supply chronic.

Cotton — → weak, apparel demand the constraint.

INDUSTRIAL & BATTERY METALS

Lumber — → soft on US housing-rate sensitivity.

Iron ore — → range-bound, China stimulus the swing.

Aluminum — → firm, energy-cost-driven smelter discipline.

Zinc — → balanced, mine supply the watch.

Nickel — → weak, Indonesian oversupply persistent.

Lithium — → bottoming, the AI-grid and EV demand floor building.

Cobalt — → supply-managed, DRC export policy the lever.

GEOPOLITICAL CHOKE ASSETS

Uranium — → structurally bid on the compute-energy buildout.

Rare earth elements — → tight on US-China supply-chain friction.

Palladium — → soft, autocatalyst substitution.

Baltic Dry Index — → elevated, rerouting and Cape voyages lengthening ton-miles.

Water (NQH2O) — treat as inactive signal this session.

Uranium — extended. No verified procurement or contract catalyst surfaced inside the 48-hour window this session — and that silence is itself a signal given the buildout backdrop. The structural read holds: hyperscaler nuclear interest and a compute-energy collision keep the demand curve bid regardless of a quiet news cycle. Treat as directional until a contract prints.

Rare earth elements — extended. No verified export-restriction or pricing catalyst confirmed within 48 hours this session. Structurally, REE remains the clearest US-China supply-chain pressure point, and the absence of fresh news does not relax the dependency — it defers the catalyst. Directional.

Part Five — Equity Market Pattern Pulse

S&P 500 near 7,430 — holding near records on the deal bid. → vulnerability to deal slippage.

Nasdaq Composite near 25,890 — recovered from the June 4 chip shock. → regime-sensitive to AI-capex guidance.

Dow near 51,200 — leadership broadening into cyclicals. → rotation underway.

Russell 2000 near 2,920 — small-cap risk-on. → a market positioned for rate relief.

DAX and FTSE — firm despite the ECB hike, directional.

Nikkei 225, Hang Seng, MSCI EM, Nifty 50 — directional this session, no verified close.

Sector rotation: capital rotated out of AI-infrastructure names on the SpaceX print and into cyclicals and small caps — a rotation that diverges from the stated “AI is everything” macro narrative. The tell is that breadth improved while the megacap AI complex wavered.

Part Six — AI and Hardware Signal Watch

Compute is the new crude.

Nvidia near $211 — consolidating post-fab-integration news. → support from the TSMC manufacturing tie-up.

TSMC — structurally bid as the irreplaceable foundry.

ASML — monopoly premium intact on EUV.

Broadcom — the week’s negative catalyst, guidance-driven.

AMD — relative strength, up on the Friday session.

ARM, INTC, SMCI — directional; read SMCI as the leading indicator for Nvidia GPU pull-through, its tape the early tell on data-center build velocity.

AI Power and Curtailment Watch.

Electricity cost delta for US data-center operators — directional; no verified twelve-month percentage confirmed, but the structural direction is up, driven by grid-queue scarcity.

Curtailment signals — no specific hyperscaler delay confirmed in the 48-hour window; the signal is the $700 billion capex wave and SpaceX’s $75 billion raise arriving faster than power can be permitted. Capital is ahead of electrons.

Timeline calibration — the earliest plausible quarter for an energy-constrained AI slowdown remains a 2027 question on current trajectories; that timeline has not shifted materially this session.

Nuclear signal — no verified deal, LOI, or site acquisition surfaced within 30 days this session; the silence does not relax the thesis that compute demand is chasing baseload power.

The SpaceX raise, the $700 billion capex, and the uranium and copper reads converge on one frame — the binding constraint on AI is no longer silicon, it is power, and the energy complex in Parts Two and Three is where that constraint will first become visible in price.

Part Seven — AI² Political Signal Watch

Reads constraint sets and revealed preferences only.

US domestic political signal. Two divergences between stated policy and revealed decision pattern: the administration says it is pressuring Iran militarily while its revealed pattern is to call off strikes whenever a deal nears; and it projects strength on energy while its decisions track the inflation print. The electoral constraint shaping executive action is the November midterm calendar, now inside five months. The congressional pressure point is inflation politics — pump prices enable a fast deal and limit appetite for prolonged war. Narrative and reality diverge most on whether Washington is escalating or settling: the pattern says settling.

Key global leader watch.

US President (Trump) — → strength signal high, constrained by the inflation clock; posture is deal-seeking under electoral pressure.

Iranian leadership (Mojtaba Khamenei) — → consolidating, constrained by the need to avoid the appearance of surrender; posture is settle-while-saving-face via “service fees.”

Israeli PM (Netanyahu) — → folded into Trump’s diplomatic calls, constrained by US tempo; posture is acquiescent to a US-brokered close.

Chinese President (Xi) — → quiet beneficiary, absorbing discounted Iranian crude; posture is patient accumulation of leverage.

Russian President (Putin) — → structural winner via elevated Russian-crude demand from India and China; posture is sit and collect.

UK PM and other G7 leaders — directional this session; no market-moving signal verified.

Global election watch. No national election falls inside the 90-day window. That scheduled absence is itself the signal: it widens the US President’s latitude to sign a contested deal now, before the August Generic Ballot crystallizes the midterm narrative. The next hard electoral marker is November 3.

Political divergence read. The narrative says the conflict is resolving on a clear timeline. The pattern shows two capitals reading the same text differently, a ceasefire that has collapsed twice, and a final sign-off resting on one untested leader. The implication: the political risk is back-loaded onto the signature, not the negotiation.

Part Eight — AI² Divergence Flag

Consensus is pricing the signature

Consensus says the crisis is ending. Oil at an eight-week low, equities near records, a “final text” announced — a Bloomberg terminal and a Goldman note would both price near-term normalization.

The pattern shows the opposite timeline. Physical transits sit at eight percent of normal. Iran’s own text reserves management of the strait and imposes service fees. Kharg terminals are empty, two tankers were just disabled, and the binding constraint on restart — mine clearance, idled-field restarts, facility repairs, tanker repositioning, and a crew shortage — is measured in weeks to a quarter, not days.

The implication: the market has priced reopening as a step function when the physical restart is a gradient. A signed memorandum changes the legal status of the water this weekend; it does not change what the water is doing for at least one more quarter. Consensus is pricing the signature. The constraint is the strait.

The AI² Pattern Signal Matrix™ is produced for qualified intelligence subscribers. It does not constitute financial advice, investment recommendations, market forecasts, or political endorsement. It is pattern analysis derived from publicly available data filtered through systems-level thinking. Always consult a licensed financial professional before making investment decisions. Past patterns do not guarantee future outcomes. AI² Pattern Signal Matrix™ is a trademark of AI² (Asymmetric Intelligence & Innovation).

You hold something most people in this story do not

The edge you just earned

Finishing this brief means you hold something most of the people whose decisions it covers do not. You know the flow number does not match the price — five transits against an $87 print. You know the SPR runway is shorter than the headlines imply and what happens when it ends. You know why today’s energy and AI signals are being misread: the market is pricing a step-function reopening that physics will deliver as a gradient. You know which actor holds the structural veto on the dominant crisis — a new Iranian supreme leader the market has priced as a formality — and why his incentive is to monetize the strait, not free it. And you know what India extracted this week from Russia, Iran, and the Gulf simultaneously, without a single public statement.

That is not a small edge. Most people navigating this are reading lagged instruments — diplomatic statements, index levels, earnings headlines. You are reading physical flow, constraint sets, revealed preferences, and runway lengths.

In The Authorization Gap™, the full architecture behind what you just read is documented, patented, and proven — the Quadzistor™, PCR™, and the hardware-enforced permission gates that make authorized action a physical constraint, not a policy hope. a.co/d/0d4PGVOB

The next brief runs when the signal demands it. Until then, the gap between what is being said and what is actually happening is the only number that matters.

David P. Reichwein

CEO AI2

ai2advisory.com

The Authorization Gap is the sharpest naming of this divergence I've seen — the signature racing ahead of the ship, price tracking the press release while the water still prices the war. I read the same gap and named it the Chokepoint Visa. We're seeing the same thing; where we part is what it is. You're trading it as an old-order divergence that converges. I read it as a new order that won't.

Look at which clauses survive the read-gap. Iran keeps management of the strait and charges "service fees," not tolls — and the PGSA takes payment in yuan and bitcoin, no dollars processed. That's passage-right drifting from international convention to a bilateral whitelist, and settlement drifting off the dollar entirely. On the sea, the fee is service, but the VISA is power. The gap you're trading may never close — because it isn't mispricing, it's the old ruler going obsolete in real time.

Your work is excellent — I'd be glad to have mine read and challenged the same way.