AI² GLOBAL SYSTEMIC INTELLIGENCE BRIEF

Day 82 — Thursday, May 21, 2026

THE ONE PATTERN THAT MATTERS TODAY

The 30-year Treasury at 5.20% — its highest since 2007 — and the S&P 500 at 7,400 are printing simultaneously while the Strait of Hormuz runs at 2% of its pre-war baseline on Day 82. The FOMC majority is now leaning toward rate hikes, but Trump is demanding cuts from a brand-new Fed Chair who has not yet held a single meeting — the Authorization Gap™ made visible in sovereign debt: the system is acting on one assumption while the structural constraint set demands the opposite. Three supertankers transited Hormuz yesterday and oil dropped 5%; the entire rate and inflation thesis pivots on a chokepoint that is still, by every measure, closed.

One Chart that Matters:

Story 1 — Hormuz at 2%: The Chokepoint That Refuses to Resolve

What happened: Straits.live confirmed 2 vessel transits on May 20 against a pre-crisis baseline of 95 per day — 2% of normal flow, Day 82 of effective closure. War-risk insurance premiums are running at 8x pre-crisis, with 6 P&I clubs having withdrawn cover. Three supertankers were spotted in satellite data crossing the strait, triggering a 5% single-session drop in Brent on diplomatic optimism.

Why it matters: Three supertankers represent a data point, not a reopening. The ADNOC CEO has stated full recovery in Middle Eastern oil flows is unlikely before late 2027 — a statement that has received almost no coverage relative to its strategic weight. The gross disruption is 20 million barrels per day theoretical; the net disruption, accounting for Cape of Good Hope rerouting, SPR draws, and shadow fleet arbitrage, is significantly lower — but the SPR is now down 6.6% year-on-year, a runway that is compressing, not expanding.

The hidden driver: Iran’s negotiating team understands that every day of closure extracts sovereign revenue from Gulf states without a single additional Iranian asset being struck — the chokepoint is doing diplomatic work that no missile can replicate.

Story 2 — Trump’s “Final Stages”: The TACO Doctrine Reaches Its Credibility Ceiling

What happened: President Trump told reporters the US is in “final stages” of Iran negotiations, triggering the single-session Brent drop noted above. Pakistan is mediating. Iran’s 14-point proposal is under US review. The core sticking points: zero enrichment (US demand) vs. a time-limited enrichment cap (Iran counter), and Hormuz reopening sequencing relative to sanctions relief.

Why it matters: Trump has now set and missed deadlines on March 21, March 23, and April 7. This is the fourth “final stages” signal since the April 8 ceasefire. The market still moves on each one — which tells you the market’s institutional memory is shorter than Iran’s negotiating patience. The enrichment gap — US demanding zero, Iran offering five years, US counter-proposing twenty — is not a rounding error. It is a structural incompatibility.

The hidden driver: Iranian negotiators are running out the clock toward a US midterm cycle that begins pressuring Republican incumbents in early 2027 — the political reserve runway in Washington is shorter than it appears.

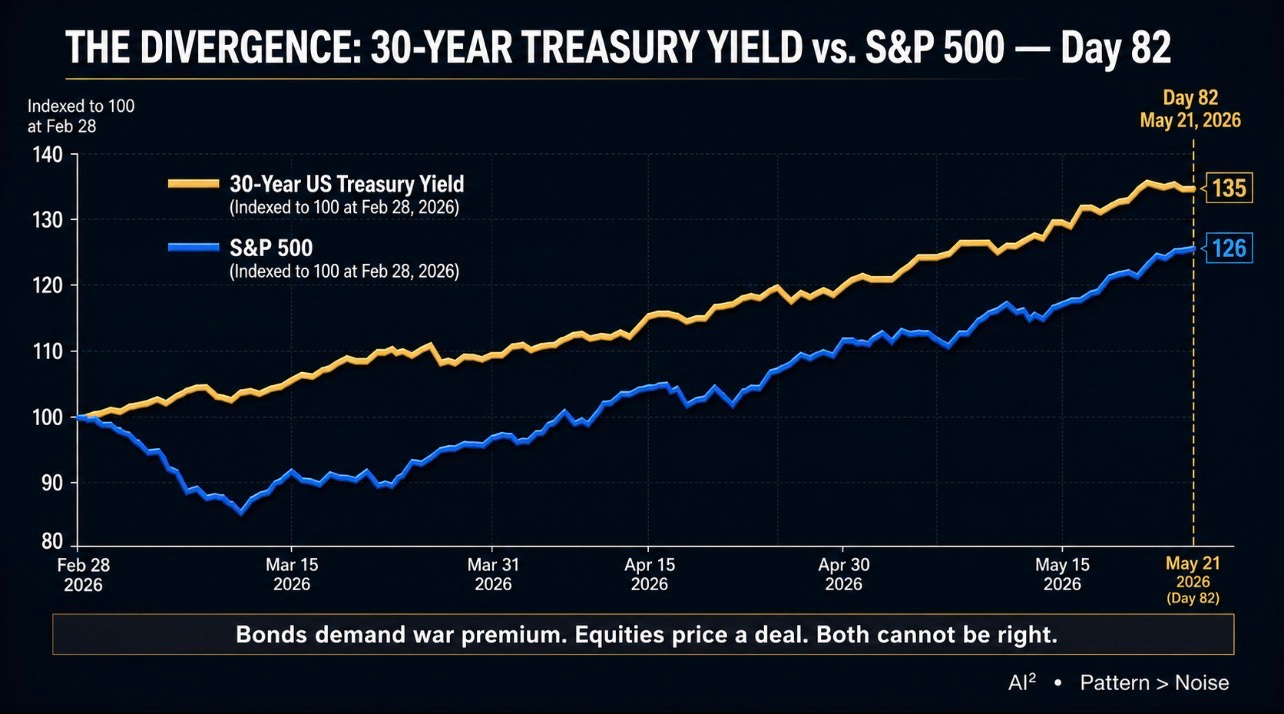

Story 3 — The 30-Year Treasury at 5.20%: The Bond Market Is Calling Someone’s Bluff

What happened: The 30-year US Treasury yield hit 5.20% on May 19, its highest level since 2007. The 10-year reached 4.67%. FOMC minutes from the April 27–28 meeting, released this week, confirmed that a majority of Federal Reserve officials now anticipate rate hikes if the Iran war continues driving inflation. CPI came in at 3.8% annualized in April — highest since May 2023.

Why it matters: The bond market and the equity market are simultaneously pricing irreconcilable scenarios. Bonds are pricing persistent inflation, fiscal deterioration, and potential rate hikes. Equities are pricing an AI earnings supercycle and a diplomatic Hormuz resolution. These two cannot both be correct. When they diverge this sharply, history suggests one of them snaps — and the bond market, which trades on approximately ten times the daily volume of equities, has historically been the more accurate leading indicator.

The hidden driver: Kevin Warsh, confirmed as the new Fed Chair this week, has not yet held a single FOMC meeting. He inherits the most divided Federal Open Market Committee in more than thirty years and a president who is publicly demanding rate cuts while the market demands rate hikes. His first meeting is the most consequential first meeting of any Fed Chair since Volcker.

Story 4 — Nvidia Beats at $81.6 Billion: The AI Infrastructure Thesis Holds — With One Footnote

What happened: Nvidia reported fiscal Q1 2027 revenue of $81.62 billion against estimates of $79.2 billion, EPS of $1.87 versus $1.76 expected. Q2 guidance of $91 billion came in slightly below the most aggressive analyst targets. The company announced a dividend increase. CEO Jensen Huang stated his view that China’s AI market will eventually open.

Why it matters: Fourteen consecutive quarters of sequential revenue growth is not momentum — it is a structural confirmation of AI infrastructure capex as a multi-year committed spend. The Q2 guidance “miss” is a function of expectation inflation, not demand deceleration. The China commentary matters: Nvidia is signaling that it views current export restrictions as temporary, which is a direct read on where Jensen Huang thinks the US-China relationship is heading.

The hidden driver: Custom ASIC growth from hyperscalers (Google, Amazon, Microsoft) is projected at 44.6% in 2026 versus 16.1% for GPUs — the market is beginning to bifurcate between Nvidia’s platform and custom silicon, a divergence that will not show up in Nvidia’s numbers for 12–18 months but will define the competitive landscape in 2028.

Story 5 — The S&P 500 at 7,400: Record Highs in a War Economy

What happened: The S&P 500 closed at approximately 7,398–7,432 this week, near all-time highs set May 13. The index has gained 26.57% year-over-year. The top 10 holdings now represent 41% of total market cap — 14 percentage points above the dot-com peak. 84% of S&P 500 companies reporting Q1 2026 results beat EPS estimates.

Why it matters: The market is pricing an AI earnings supercycle, a Hormuz deal, and benign rates simultaneously. Each of those three assumptions is under active challenge by verified real-world data. The passive indexing feedback loop — where every dollar into an S&P index fund becomes a forced allocation to the same 10 names — has created price momentum that is structurally disconnected from the risk environment. This is not 2000’s Pets.com. These are real earnings. But 41% concentration with the bond market screaming inflation is not a comfortable position.

The hidden driver: Institutional positioning is still underweight energy and overweight technology relative to the macro environment — a rotation into the former and out of the latter has not happened yet, which means the eventual rebalancing will be non-linear.

Story 6 — Kevin Warsh Confirmed: The Most Consequential Fed Appointment Since Volcker

What happened: Kevin Warsh was confirmed by the Senate as Federal Reserve Chair this week. He inherits Fed funds at 3.5–3.75%, a 30-year yield at 5.20%, a majority of FOMC officials leaning toward hikes, and a president demanding cuts.

Why it matters: Warsh is entering a classic central bank trap: cutting rates would validate Trump’s political pressure but would be seen by the bond market as capitulation to inflation — driving yields higher and undoing any easing. Holding or hiking rates would produce a political confrontation with the executive branch but would be consistent with the bond market’s current demand. His first press conference will be more consequential than any single piece of macro data this year.

The hidden driver: The long end of the Treasury market — not Warsh, not Trump — is now de facto setting monetary policy. “Long end rates are in control,” as one major fixed income strategist stated this week. This is the deepest structural shift in US monetary governance since the 2008 crisis.

Story 7 — SPR Depletion: The Emergency Reserve Is Becoming the Operating Reserve

What happened: The US Strategic Petroleum Reserve has been drawn down 10 million barrels since the war began, now showing a 6.6% annual decline. Crude inventories have fallen for four consecutive weeks. The SPR was designed as an emergency buffer, not an operational supply management tool.

Why it matters: The SPR draw is suppressing the gross disruption figure — it is part of what makes the net disruption appear manageable. But every barrel drawn now is a barrel unavailable for a future, potentially more acute disruption event. The US is spending its emergency margin to hold the current price line.

The hidden driver: The administration is managing oil prices through SPR draws to suppress the political pain of $5 gas ahead of an emerging midterm narrative — the reserve is being used as a political instrument, not a strategic one.

Story 8 — US Gas at $5: The Consumer Price That Runs Every Other Political Calculation

What happened: US retail gasoline prices remain near $5 per gallon nationally, directly tied to Hormuz disruption and the 62% year-over-year rise in crude. The CPI print of 3.8% annualized significantly understates energy-driven household cost pressure in lower-income deciles, where transportation spending as a percentage of income is three to four times the national average.

Why it matters: $5 gas is not a macroeconomic statistic. It is a daily political event for 150 million working Americans. Every week it persists adds to the erosion of the administration’s credibility on the core promise of cost-of-living relief. The political reserve runway for the Iran war strategy is being depleted at the pump, not in the polling.

The hidden driver: Trump’s “final stages” declarations are primarily directed at domestic political audiences, not at Tehran. The signaling is about managing the gas price narrative, not closing the deal.

Story 9 — India’s Energy Arbitrage: The Silence That Is Louder Than the Noise

(See full India section below)

What happened: Indian crude imports from Russia running at approximately 1.9 million barrels per day as of May 2026 (Kpler), representing roughly 40% of India’s total crude requirements. The February 2026 US-India trade deal included Trump’s claim that India agreed to reduce Russian crude imports — a claim India has not formally confirmed.

Why it matters: India is simultaneously the world’s third-largest oil importer and the most strategically positioned fence-sitter in this crisis. It is buying discounted Russian crude at 15–20% below Brent, refining it, and exporting products to markets paying elevated prices. The arbitrage is compounding silently.

The hidden driver: The US-India trade deal created political cover for continued Russian crude imports — India can claim compliance while operationally maintaining the same purchasing pattern through different routing and documentation.

Story 10 — Iran’s 14-Point Proposal: The Gap Between the Text and the Deal

What happened: Tehran submitted a 14-point proposal to Washington via Pakistani mediation. The key divergences: Iran wants enrichment rights (even time-limited), US demands zero enrichment. Iran wants phased sanctions relief tied to Hormuz reopening. US wants Hormuz open before relief. The enrichment gap is running at 15 years: US proposes twenty-year limit, Iran counters with five.

Why it matters: The 14-point structure is a negotiating document designed to produce a negotiating process, not a deal. Iran has studied every prior nuclear negotiation cycle and knows that time-limited enrichment bans expire. The fifteen-year gap in the duration argument is not a compromise — it is a signal that Iran’s red line has not moved since the 2015 JCPOA framework.

The hidden driver: Iran’s new post-Khamenei leadership has fewer internal constraints to a deal than the prior regime but more need to show domestic audiences that sovereignty was preserved — the deal, if it comes, will be framed in Tehran as a victory, not a capitulation.

Story 11 — FOMC Minutes: The Rate Hike Majority That Nobody Is Pricing

What happened: April 27–28 FOMC minutes confirmed that a majority of Federal Reserve officials anticipate rate hikes if the Iran war continues. The Fed funds rate remains at 3.5–3.75%, held since December. Fed funds futures are now pricing a meaningfully higher probability of tightening this year.

Why it matters: A rate hike into a war-driven energy shock is the most contractionary policy scenario the US economy could face — it simultaneously raises borrowing costs and fails to address the supply-side inflation driver. The Fed cannot drill its way out of the Iran war. Rate hikes here would be fighting the wrong fire with the wrong instrument.

The hidden driver: The minutes are a message to the incoming Warsh Fed — the institutional position has already shifted, and any Chair who ignores that alignment walks into his first meeting without a majority.

Story 12 — China’s Semiconductor Defense: The Domestic Moat Deepens

What happened: The Financial Times reported this week that Beijing is taking active new measures to protect its domestic semiconductor manufacturing industry. Nvidia’s Jensen Huang, in a Bloomberg interview, described China’s domestic market as one the government must choose to protect or open — framing that signals he sees regulatory arbitrage as Beijing’s core decision variable.

Why it matters: China’s semiconductor strategy is bifurcating: restrict US imports where possible, accelerate domestic production, and use whatever access remains to extract maximum intelligence from frontier models (the Distillation War dynamic). The 50,000-account extraction methodology documented earlier this year remains the most efficient vector — and it requires no chips at all.

The hidden driver: China’s domestic chip design capability has advanced faster than Western intelligence assessments predicted — the export control strategy may already be fighting the last war.

Story 13 — Netanyahu’s Coalition Fractures: Israel’s Internal Clock Is Running

What happened: Reports this week confirm Netanyahu’s coalition is fracturing as Israel edges toward early elections. The Iran war has produced military gains but accelerating domestic political costs, including ultra-Orthodox coalition pressure on conscription exemptions and settler faction pressure on Gaza post-war governance.

Why it matters: A coalition collapse in Israel would produce a caretaker government with reduced mandate to commit to any US-Iran deal terms that require Israeli concessions — particularly on Hezbollah disarmament sequencing or Palestinian governance structures. The diplomatic window is narrower than it appears because the Israeli political clock is running independently of the Hormuz clock.

The hidden driver: Netanyahu’s personal legal exposure — ongoing corruption proceedings — means his political survival and the war’s diplomatic resolution are entangled in ways that no external mediator can fully map.

Story 14 — The Shadow Fleet and the Workaround Economy

What happened: UANI tracking shows at least 37 tankers laden with Iranian oil operating inside the Persian Gulf west of Hormuz as of May 11, with 13 Iranian-flagged tankers observed near Chabahar Port. US CENTCOM has redirected 62 commercial ships and disabled 4 since the blockade began. Eight tankers returned to port after US enforcement actions.

Why it matters: The workaround economy is functioning at partial capacity — Iranian exports are not zero, but they are severely constrained. The gap between gross disruption (20 million barrels per day theoretical) and net disruption (actual supply removal) is being absorbed by Cape rerouting, SPR draws, and shadow fleet arbitrage. But each of these absorption mechanisms has a finite runway. The workaround economy is borrowing time, not solving the structural problem.

The hidden driver: Every dark tanker that successfully moves Iranian oil is a data point that Iran uses to argue it can sustain the closure longer than Washington believes — the shadow fleet is an intelligence signal as much as a logistics operation.

Story 15 — The Cape of Good Hope Reroute: A 40-Day Detour With a 2027 Problem

What happened: The Hormuz closure has forced a near-complete reroute of Gulf-origin cargo around the Cape of Good Hope — adding approximately 40 days and 30–40% to shipping costs for Asia-bound cargoes. ADNOC’s CEO stated full recovery in Middle East oil flows is unlikely before late 2027.

Why it matters: The reroute is not a fix. It is a compression — the same oil reaches the same destinations but arrives later, costs more, and occupies tanker capacity that is no longer available for spot market flexibility. The ADNOC late-2027 timeline is the most consequential single statement made by any energy executive this week and has been almost universally underreported.

The hidden driver: Shipping companies have committed to long-term Cape reroute capacity agreements — their contractual positions now create a constituency against rapid Hormuz reopening, because reopening makes their reroute investments stranded assets.

Story 16 — The US Debt Ceiling Approaches: Fiscal Pressure Meets Bond Market Pressure

What happened: The 30-year Treasury at 5.20% reflects not only energy-driven inflation but deepening fiscal concerns. The US recorded a $215 billion April surplus (typical for the month), but the annual trajectory remains in severe deficit. Global sovereign debt stress is accelerating — the UK and European bond markets are showing correlated pressure.

Why it matters: The bond market is now simultaneously absorbing: war-driven inflation risk, Fed transition uncertainty, energy shock fiscal cost, and structural deficit concerns. When four independent risk factors converge on the same instrument, the pricing is no longer about any one factor — it is about the system’s trust in the underlying issuer.

The hidden driver: Foreign holders of US Treasuries — particularly Japan and China — are the marginal price-setters at these yield levels. Any signal of reduced foreign demand at auction would accelerate the yield move in a way that domestic monetary policy cannot offset.

Story 17 — AI Governance: The Tort Clock Is Running

What happened: No single governance event this week — but the convergence of Nvidia’s $81B quarterly revenue, the 41% S&P concentration in AI-adjacent names, and the absence of any deterministic control framework in any major agentic deployment creates the structural setup for the first major AI liability event.

Why it matters: The Authorization Gap™ is not a theoretical risk. It is the operational state of every enterprise agentic deployment running today. The lawsuit dismissed against OpenAI this week on statute of limitations grounds is not a governance victory — it is a preview of the litigation architecture that will be deployed when an agentic system causes a material harm in a high-stakes environment. The question is not whether it happens. It is which deployment produces the first verdict.

The hidden driver: The companies that have explicitly documented awareness of deterministic control alternatives and deployed without them have created the paper trail that plaintiff’s counsel will need. “Speed without brakes” generates discovery.

Story 18 — Europe’s Industrial Competitiveness: The Quiet Bleeding

What happened: European energy costs remain structurally elevated — Brent at $106 with no Gulf supply recovery before 2027 means European manufacturers are competing against Asian counterparts who have greater access to discounted Russian and non-Gulf crude. German industrial output data continues to disappoint.

Why it matters: Europe entered this crisis with limited energy storage, elevated dependency on Middle Eastern LNG, and a political coalition already under pressure from far-right parties weaponizing cost-of-living grievances. The war has amplified every pre-existing structural vulnerability simultaneously.

The hidden driver: European governments are quietly providing industrial energy subsidies that are not being publicly disclosed in their full scale — the fiscal cost of the war’s energy shock is being absorbed off-balance-sheet in ways that will surface in sovereign debt ratings over the next 18 months.

Story 19 — Pakistan as Mediator: The Quiet Power in the Room

What happened: Pakistan brokered the April 8 ceasefire and is the current primary channel for US-Iran communications. Pakistan arranged the conditional two-week ceasefire that has now been extended. The mediation role gives Islamabad access to both Washington and Tehran at the highest levels simultaneously.

Why it matters: Pakistan is extracting significant strategic value from the mediation role — IMF forbearance, quiet US tolerance of its China relationships, and enhanced regional legitimacy. This is a textbook application of strategic ambiguity: converting geopolitical positioning into concrete economic and diplomatic gain. India is watching this dynamic with significant discomfort, as Pakistani diplomatic capital is rising at the precise moment Indian-Pakistani relations are under routine pressure.

The hidden driver: Pakistan’s military leadership, not its civilian government, is running the mediation — which means the channel’s continuity is insulated from electoral cycles but vulnerable to internal military alignment shifts.

Story 20 — The SpaceX IPO Signal: The Largest Narrative Asset in the Market

What happened: Reports this week confirm SpaceX is preparing for what could be the largest IPO in history. The timing — amid Musk’s DOGE exit, Tesla narrative reset pressure, and X engagement dynamics — places the IPO preparation in a context that is as much about narrative asset management as capital formation.

Why it matters: A SpaceX IPO at the current moment monetizes the Mars/consciousness narrative at peak premium. The story is large enough that no institutional investor can ignore it and no retail participant can short it without positioning against “the future of humanity.” This is the largest single narrative-driven valuation event in market history — and it arrives at the moment of maximum concentration in the top 10 S&P names.

The hidden driver: The IPO timing is constrained by Hormuz resolution — a prolonged war and elevated rates compress the multiple SpaceX can command. Every week of closure costs the IPO valuation more than it costs the mission narrative.

SYNTHESIS SECTIONS

1. THE SYSTEM MAP

The dominant force in global markets today is a single feedback loop: the Hormuz closure drives energy prices, which drives inflation, which drives bond yields, which pressures the equity multiple, which pressures the political narrative, which creates pressure for a deal, which moves oil on the rumor, which relieves the bond pressure temporarily, which gives the equity market room to run — until the next day, when Hormuz is still effectively closed and the cycle restarts.

The second dominant force is the fiscal constraint. The US is simultaneously managing a war, drawing down strategic reserves, facing potential Fed rate hikes, and approaching a debt ceiling reckoning with a bond market that is demanding 5.20% for thirty-year money. These are not independent problems. They are the same problem viewed from different instruments.

The third force is the AI capital concentration dynamic. Nvidia at $81.6B quarterly revenue is real. The 41% S&P top-10 concentration is real. The divergence between what these companies earn and what the bond market is pricing is also real. Capital is simultaneously flowing into the highest-conviction AI thesis in history while the macro environment is assembling the most contractionary setup since 2007. These two forces will not coexist indefinitely.

The political force threading through all of this is the gap between Trump’s stated positions and his actual constraint set. He demands rate cuts while the bond market demands hikes. He declares “final stages” while Hormuz transits at 2%. He claims India agreed to cut Russian crude while India maintains 1.9 million barrels per day. The Authorization Gap™ is not only an AI governance concept. It is a description of this administration’s operating posture: authorization claimed, control absent.

2. PATTERN RECOGNITION

The repeating structure visible today is the political deadline inflation cycle: a credible threat is issued, a deadline is set, the deadline passes without enforcement, a new deadline is set with new framing, the process repeats. This is not unique to the Iran negotiation. It has characterized the tariff cycle, the NATO burden-sharing cycle, and the debt ceiling cycle. Each repetition slightly reduces the credibility premium of the next threat — but markets continue to trade the rumor because the optionality of resolution is worth more than the certainty of stalemate.

What is accelerating: bond market pressure on long-duration assets, the gap between AI earnings and macro fundamentals, India’s strategic ambiguity dividend, and the pace at which Iran is extracting negotiating value from time.

What is breaking: the credibility of US diplomatic deadlines, the SPR as a shock absorber, European industrial competitiveness, and the assumption that monetary policy can address supply-side inflation.

3. HISTORICAL ANCHORING

The most precise historical analog for the current moment is not the 1973 oil shock, which was a supply cartel action. It is the 1987 Tanker War — a period in which US naval forces escorted Kuwaiti tankers through a contested Gulf while oil prices and diplomatic negotiations ran on parallel tracks. The 1987 analog applies because: the chokepoint was never fully closed but was sufficiently disrupted to sustain price elevation; the diplomatic resolution came through exhaustion and back-channel sequencing rather than public agreement; and the equity market continued to advance until it abruptly did not, in October 1987.

The divergence from the 1987 analog: today’s closure is more complete (2% vs. perhaps 70% flow in 1987), the AI earnings cycle provides an independent equity support that did not exist in 1987, and the bond market starting point — 5.20% on the 30-year — is materially higher than any point during the 1987 episode. The October 1987 crash was triggered by the intersection of elevated bond yields, equity overvaluation, and a single geopolitical escalation. The setup today contains all three preconditions. The timing is not predictable. The structural conditions are.

4. FORWARD PROJECTION

If the current trajectory continues for thirty days: Brent holds above $100, the 30-year yields 5.3–5.5%, the new Fed Chair delivers hawkish forward guidance at his first meeting, equity markets face a 10–15% correction as the rate-hike probability reprices into multiples, and the Hormuz negotiation enters a fifth “final stages” cycle with diminishing market response. India quietly absorbs more Russian crude as Gulf supply remains constrained. Pakistan extracts additional concessions from both Washington and Tehran. China accelerates domestic semiconductor production behind the cover of the crisis.

The second-order effects: European sovereign spreads widen as energy subsidy costs surface, US consumer confidence deteriorates as $5 gas persists through summer driving season, and the SpaceX IPO is delayed pending rate stabilization.

The scenario that breaks the trajectory: a credible partial Hormuz reopening — not a deal, but a verified, sustained increase in transits to 30–40% of pre-war baseline. This releases the bond pressure, gives Warsh room to hold at current rates, and allows the AI earnings thesis to re-assert without macro headwinds. Three supertankers is not that signal. Forty is.

5. THE LOCAL LENS

UNITED STATES

Americans are living in a war economy without a declared war. Gas at $5 is not an abstraction — it is a daily tax on every commuter, every delivery driver, every small business owner whose margins run on fuel costs. The administration is managing the political pain through SPR draws and “final stages” declarations, but the runway on both instruments is compressing. Kevin Warsh now faces the most consequential first months of any Fed Chair in a generation: a majority of his own committee is leaning toward hikes, the president is demanding cuts, and the bond market is setting policy whether anyone in Washington acknowledges it or not. The midterm narrative — which formally begins in 2027 but politically begins the moment gas prices determine suburban voting patterns — is already forming against the administration on cost-of-living grounds.

EUROPE

European governments are managing an energy crisis that has no near-term resolution path. Brent above $100 with the ADNOC late-2027 recovery timeline means European manufacturers face structurally elevated input costs for at minimum 18 months. German industrial output is the leading indicator — when it deteriorates, the broader European competitiveness story deteriorates with it. Far-right parties across France, Germany, Italy, and the Netherlands are converting energy cost pressure into electoral momentum with a coherence and speed that incumbent center governments cannot match. The political risk is not that they take power immediately — it is that the threat of their taking power constrains the fiscal and energy policy options of the incumbents who remain.

ASIA

China is running the most sophisticated dual-track strategy of any major power in this crisis: public neutrality, private arbitrage. It is absorbing reduced Gulf crude at elevated prices, protecting its domestic semiconductor industry through regulatory measures, extracting AI capability from Western frontier models through systematic querying, and positioning its currency as an alternative settlement mechanism for sanctioned energy trades. Japan and South Korea face acute vulnerability — both are heavily Gulf-dependent importers with limited domestic energy production, and both are watching their industrial competitiveness erode in real time. Southeast Asia is positioning as a non-aligned beneficiary: Malaysia, Indonesia, and Vietnam are all quietly offering alternative routing, transshipment, and refining capacity to parties on both sides of the sanctions regime.

MIDDLE EAST

The post-war regional order is being written in real time, and the authors are not the ones with the largest militaries. Saudi Arabia is managing an OPEC+ coalition that is increasingly fractured — members with sanctioned or restricted output (Russia, Iran, Iraq, Venezuela) are operating outside quota discipline while the Kingdom absorbs the role of swing producer to a market it cannot fully control. The Gulf sovereign wealth funds are reallocating away from US Treasuries at precisely the moment the US needs foreign demand to hold yield levels. Qatar’s LNG position has become more valuable than any party anticipated — European buyers who dismissed LNG as a transitional fuel are now signing decade-long contracts at elevated prices.

INDIA

Energy arbitrage: India is running approximately 1.9 million barrels per day of Russian crude imports (Kpler, May 2026), representing 40% of total crude requirements. This crude prices at 15–20% below Brent on delivered basis. With Brent at $106, the arbitrage is generating a terms-of-trade gain of approximately $15–20 per barrel on nearly 2 million barrels per day — a compounding economic advantage that runs silently while the world watches Hormuz. The US-India trade deal’s Russian crude language has not altered the operational flow; India’s Ministry of External Affairs has maintained its standard formulation that energy security for 1.4 billion people is the supreme priority.

Refined product export dynamic: Indian refiners are processing discounted Russian crude and exporting refined products — diesel, jet fuel, gasoline — to European and Asian markets paying elevated post-Hormuz prices. This is the most valuable position in the current energy architecture: buying at a discount and selling into a premium market. The margin compression that would normally kill this trade has not arrived because the Gulf supply disruption has elevated the product price floor globally.

Strategic ambiguity dividend: India is extracting concrete value from four simultaneous relationships this week. From the US: trade deal concessions and technology transfer flexibility. From Russia: discounted crude at scale. From the Gulf states: continued term contract supply for diversity. From Pakistan’s mediation role: the signal that regional diplomatic architecture is not India’s to control, which itself motivates India to accelerate its own regional influence investments.

Domestic inflation and political exposure: The Modi government’s arbitrage gains at the sovereign level are not fully passing through to retail consumers. Indian retail fuel prices remain elevated because the government is recovering refinery subsidies rather than transmitting the full discount. The political tension is most visible in state election cycles — where opposition parties are effectively campaigning on the gap between India’s energy arbitrage gains and consumers’ actual pump prices.

Semiconductor and AI positioning: India’s domestic AI and chip design ecosystem is advancing faster than 18 months ago — Tata’s semiconductor fab announcement, the growth of Bangalore as a global AI research hub, and India’s positioning in the global GPU allocation queue all represent structural gains. The current global semiconductor export control environment benefits India net — it faces fewer restrictions than China while gaining access to US technology transfer through the trade deal framework.

Strategic ambiguity risk: The most fragile bilateral relationship in India’s current posture is with the US on the Russian crude question. Trump claimed India agreed to cut Russian imports. India did not confirm. This is a functional misrepresentation sitting in the diplomatic record — and when it surfaces explicitly, likely in a Congressional hearing or sanctions enforcement action, India will be forced to either formally confirm a commitment it has not operationally honored or formally deny one the US president stated publicly. That forcing function has not arrived yet. When it does, the ambiguity resolves — and the resolution will not favor both sides simultaneously.

GLOBAL SOUTH AND EMERGING MARKETS

The systematically underweighted story is Egypt. Egypt is simultaneously experiencing: Suez Canal revenue collapse (both major maritime corridors blocked), tourism disruption from regional conflict, IMF program pressure, currency devaluation, and food import cost inflation driven by elevated energy-linked shipping costs. The Egyptian pound has depreciated significantly, the government is drawing down reserves to defend the currency, and the social pressure on the el-Sisi government is building in ways that the Western analytical community is almost entirely ignoring because Egypt does not register as a “crisis” until it becomes one suddenly. The 2011 analog — where a government that appeared stable collapsed within weeks of visible popular mobilization — is not a prediction. It is a risk that is priced at near zero when it should be priced meaningfully above zero.

6. THE BLIND SPOT CHECK

This brief has assumed that the US-Iran negotiation is the primary diplomatic dynamic shaping Hormuz resolution timing. It may not be. The most underanalyzed factor is China’s role as a back-channel interlocutor with both parties. China has structural interests in a Hormuz reopening — its Gulf crude imports are heavily disrupted — but it also has structural interests in a prolonged US military commitment in the Middle East that keeps Washington occupied and limits its bandwidth for Indo-Pacific positioning. If China is quietly communicating to Tehran that it can absorb the supply disruption through Russian alternatives longer than Washington can sustain political support for the operation, the Iranian negotiating calculus looks entirely different from what this brief has described. The assumption embedded in today’s analysis is that Iran is negotiating toward a deal. It is equally possible that Iran is negotiating toward a prolonged process that serves Chinese strategic interests at the cost of Iranian economic pain — and that the Chinese have provided assurances of compensation that are not visible in any public data source.

All data verified. Producing V12.3b.

AI² PATTERN SIGNAL MATRIX™ — V12.3b

Day 82 — Thursday, May 21, 2026

Pattern Signal Matrix · Restricted Distribution · Paid Tier